Summary

- A major policy redesign produces modest emissions gains at best. The MOU fundamentally reshapes climate policies affecting more than 40 per cent of Canada's emissions, yet emissions outcomes remain close to today's trajectory in the best case and above it in the worst.

- Price fixing is not fixing the market. The MOU adds elements designed to strengthen Alberta's carbon market while simultaneously weakening market fundamentals. Benchmark tightening rates are cut in half significantly reducing compliance demand, while the price floor's design shifts the system away from market-driven price discovery toward fixed prices. The result is a floor asked to do too much and designed to deliver too little.

- The emissions math barely changes. Expanded pipeline capacity and higher oil production add roughly 20 megatonnes of annual emissions that won't be fully offset by the MOU's other policy changes, leaving Canada's overall emissions trajectory high well into mid-century.

- Markets are pricing in weakness. Early Alberta carbon market signals suggest market participants are pricing in materially looser market conditions, with credit prices down since the MOU was finalized.

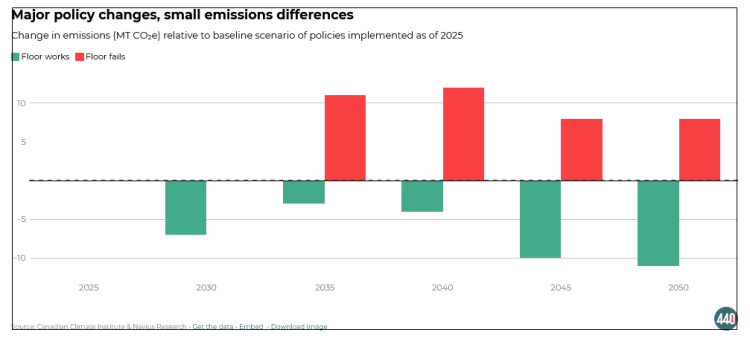

New modelling completed with Navius Research finds that the Canada-Alberta Memorandum of Understanding (MOU) agreement weakens the ability of industrial carbon pricing to materially reduce emissions, while enabling higher emissions from increased oil and gas production ultimately keeping Canada's emissions on a high trajectory through the middle of the century. Across modelled scenarios, annual emissions range from roughly 7 megatonnes below, to 9 megatonnes above, what existing policies would have delivered before the MOU was negotiated.

The MOU fundamentally redesigns Alberta's industrial carbon market, which covers about 25 per cent of national emissions. It introduces a regulated price floor, changes emissions benchmark tightening rates, commits to more pipeline capacity and decarbonization investments, and reshapes the investment incentives facing large emitters nationally. All told, the changes affect more than 40 per cent of Canada's national emissions. Despite the scale of the policy redesign, the difference in emissions between scenarios is negligible whether the MOU's price floor holds or fails. In both cases, emissions remain close to today's pathway, leaving Canada's long-term emissions trajectory much higher than it would be with stronger, cost-effective policy changes, as we have previously noted.

What we modelled

We modelled a comprehensive package of MOU changes against a reference case reflecting pan-Canadian carbon policies as implemented in 2025: Alberta's industrial carbon price frozen at $95 per tonne with benchmark tightening rates as legislated, Saskatchewan at an industrial carbon price of zero, the federal output-based pricing system applying elsewhere, the Clean Electricity Regulations in force nationally, and methane regulations achieving 75 per cent reductions by 2030. Other federal and provincial climate policies are held constant (see our previous analysis of the federal climate plan for a complete list). This provides the reference case for Canada's emissions trajectory before the MOU.

From that reference case, we modelled two MOU scenarios. Both implement the MOU's emissions benchmark tightening rates for Alberta's large emitters that cut the current rates by more than half. That reduces compliance demand for carbon credits by 30 per cent in 2030 and 60 per cent in 2040. Both MOU scenarios also extend the Clean Electricity Regulations to Alberta with extended end-of-life provisions for gas power (we assume to 35 years from 25 years), increase renewable generation in Alberta, add 1.4 million barrels per day of new oil production to fill expanded pipeline capacity, and include generous carbon capture subsidies and investment tax credits.

The scenarios differ only in how carbon credit prices are administered. In the first scenario, the MOU's price floor fails and the market settles into its natural equilibrium. In the second, the MOU's administered price floor is binding, requiring credits to be retired at or above the regulated floor beginning in 2030. Credits issued prior to 2027 are exempt from the floor and are carried over under the new system until they are used or expire, while credits issued after 2027 are subject to the floor.

Even though the MOU sets a minimum price, both of these scenarios are material given that 1) the tightening rates specified are inconsistent with the minimum price; and 2) the mechanism by which Alberta is proposing creates a superficial minimum price rather than addressing market fundamentals (more on this below).

National emissions stay close to their pre-MOU trajectory

A key reason we find minimal emissions benefits from the MOU is that the additional emissions associated with expanded pipeline capacity and higher oil production roughly 20 megatonnes annually are not fully offset by the MOU's other policy changes to Alberta's already-weakened industrial pricing system. Even under the best-case scenario with a functioning price floor and major investments in carbon capture, the net emissions benefit of the agreement would be modest.

A functioning price floor design makes a difference. By 2040, a floor working as intended reduces emissions by roughly 16 megatonnes relative to a scenario where the floor fails, growing to 19 megatonnes by 2050. Emissions gains early in the simulation remain uncertain, as roughly two years' worth of pre-2027 credits priced below the floor remain available for compliance, delaying the impact of the floor. As that stock is depleted or expires, prices remain pinned near the floor. Firms continue to have ample compliance options beyond abatement, keeping costs low while limiting incentives to reduce emissions. The result is a small net decrease in emissions below current projected levels.

Price fixing is not fixing the market

The more important finding is what happens when the floor fails. With weaker benchmark tightening and insufficient credit scarcity, emissions rise above today's projected pathway by roughly 11 megatonnes by the mid-2030s. Rather than improving outcomes, a weak floor implementation would leave Canada's emissions worse off than under today's policies.

This scenario is not hypothetical. Three design choices in Alberta's proposed implementation of a minimum price compound the underlying weakening in policy stringency:

- Credits issued before 2027 are exempt from the floor entirely, leaving a substantial stock of lower-cost credits available after 2030, allowing firms to meet compliance obligations without facing the intended floor price well into the early 2030s the critical window to begin sending investment signals.

- The system creates layers of differently priced credits based on when they were issued. That will create a hierarchy of compliance options that firms work through in order of cost, keeping prices pinned near the floor given the surplus of available credits, including a large and growing bank of floor-priced offsets.

- With benchmarks set loose enough that many facilities outperform them, and investment credits adding to overall supply, credits available at or near the floor price are abundant and renewing annually. The floor maintains prices but the underlying signal to abate is lost. Price maintenance does not translate into emissions reductions and instead the system mostly delivers paper compliance rather than cutting emissions.

Taken together these choices mean the market never tightens enough to let prices rise above the administered minimum on their own. Sustaining the floor requires more than setting a price, it requires continuously monitoring, verifying and enforcing prices against market conditions that don't support prices above the floor.

The MOU also introduces carbon contracts for difference (CCfDs) to support investment certainty. While useful for individual projects, they do not address the underlying lack of market scarcity. Taking the reported cap liability at face value, roughly $16 per tonne of protection looks to be at risk based on market prices under the floor.

A well-functioning price floor acts as insurance. Under the MOU, that floor becomes load-bearing. Instead of supporting a functioning market, the floor increasingly substitutes for one.

A major redesign with little emissions upside

Relative to today's policy environment which already includes a weak industrial carbon market in Alberta, a zero industrial carbon price in Saskatchewan, and the current federal benchmark applied elsewhere in Canada the modeled emissions outcomes of the MOU are at best modest.

The result reflects a series of forces that push and pull emissions in different directions. Methane and clean electricity regulations, renewable generation, and potential reductions associated with the proposed Oil Sands Alliance carbon capture projects improve emissions outcomes. At the same time, weaker carbon market stringency reduces the effectiveness of carbon markets nationally, while expanded pipeline capacity and higher oil production add roughly 20 megatonnes of additional emissions pressure to be offset.

Early carbon market signals are broadly consistent with this finding. Alberta credit prices have dropped since the MOU was finalized, suggesting market participants are pricing in materially looser market conditions.

The end result is a major policy intervention that leaves Canada's long-term emissions trajectory largely where it was before the MOU agreement was finalized. It results in negligible changes to a system already weakened.

Our team at 440 Megatonnes will be doing additional emissions modelling in the near future to fully assess Canada's policy options moving forward.

Dave Sawyer is Principal Economist and Head of 440 Megatonnes at the Canadian Climate Institute.